Key takeaways

- Mean reversion strategies look for stretched price that is likely to rotate back toward value, but the better versions require context, exhaustion evidence, and disciplined invalidation so traders are not simply fading strong trend pressure. The real job is to define the location, trigger, and invalidation clearly enough that two disciplined traders would make roughly the same decision. One of the first numbers to define is top-down timeframe stack: Daily or 60-minute for location, 5-minute or 1-minute for execution.

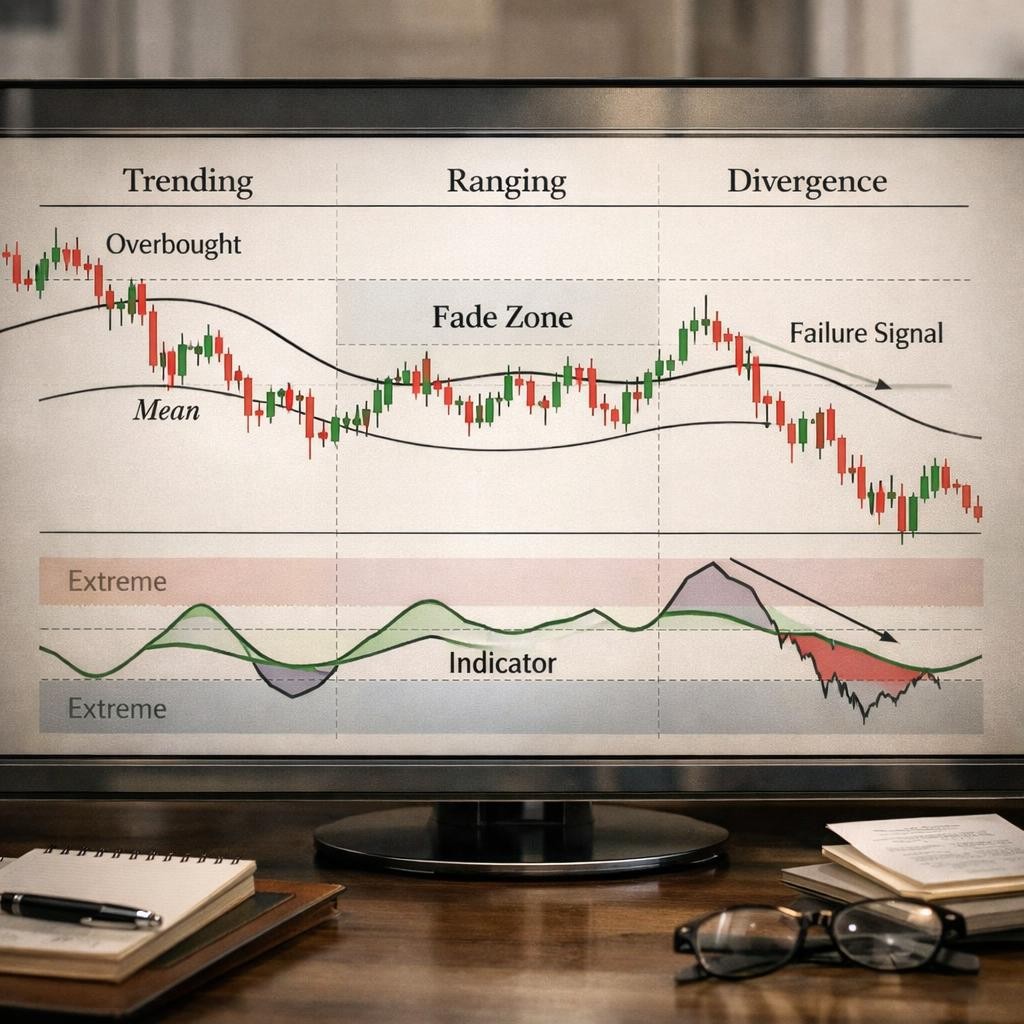

- Mean reversion works best when price is stretched relative to value, structure, or volatility and the trend is no longer cleanly expanding

- Top-down timeframe stack: Daily or 60-minute for location, 5-minute or 1-minute for execution.

- A common failure is fading a clean trend without evidence of exhaustion.

Mean reversion strategies look for stretched price that is likely to rotate back toward value, but the better versions require context, exhaustion evidence, and disciplined invalidation so traders are not simply fading strong trend pressure. The real job is to define the location, trigger, and invalidation clearly enough that two disciplined traders would make roughly the same decision. One of the first numbers to define is top-down timeframe stack: Daily or 60-minute for location, 5-minute or 1-minute for execution. This guide keeps the topic practical. Instead of circling the idea in broad terms, it moves through the actual decision chain: what the topic is, which rules matter, which numbers have to be defined early, how the setup is applied, what usually breaks, and how the session should be reviewed afterward.

For mean reversion trading strategy, the useful version is the one a trader can explain from the chart, the note, the sizing worksheet, or the alert payload without inventing missing context after the move.

What the setup is actually measuring

A trader should be able to point to mean reversion trading strategy how traders fade stretched moves without catching a falling knife, mean reversion strategy, fade stretched move, and failed breakout fade before trusting the setup with normal size. If those nouns are not visible in the chart note, payload, sizing worksheet, or review entry, the topic is still too vague to trade cleanly.

That is what separates a topic from a label. The article has to leave the trader with something observable to verify: a level, a field, a stop distance, a review question, or a no-trade condition that can still be identified while the session is unfolding.

Use the topic to answer one blunt question before the trade: Was the move stretched relative to something concrete? If the answer stays fuzzy, the setup has not earned risk yet.

Prerequisites and context before the trade

Before the trigger matters, the trader needs the surrounding context written clearly enough that another operator could explain why the setup is valid, weak, or inactive.

Context check 1

Mean reversion works best when price is stretched relative to value, structure, or volatility and the trend is no longer cleanly expanding. This should be visible before the trade, not discovered by replaying the chart later.

If this prerequisite is missing, the trade usually becomes harder to size, harder to manage, and easier to rationalize after the fact.

Context check 2

The edge comes from context and confirmation, not from a desire to pick tops or bottoms. If the trader cannot point to this condition before entry, the setup is still too loose to trust.

When this prerequisite is skipped, weak entries often look acceptable right up until the review exposes the missing context.

Context check 3

The strongest mean-reversion trades usually happen in balanced markets, overextended bursts, or failed breakouts. Treat this like a written prerequisite, not a feeling that gets filled in after the move.

Missing this prerequisite usually shows up later as late entries, wider stops, or a note that cannot explain why the trade was valid.

Context check 4

A stretched move can stay stretched longer than an impatient trader expects. This belongs in the plan before the session opens so the trade can be filtered quickly under pressure.

A missing prerequisite here usually means the trader is relying on memory or optimism instead of a rule that can survive speed.

The decision rules that separate clean reads from noise

These are the rules that should change the trade or the no-trade decision before execution begins.

If a rule does not change size, timing, routing, or the decision to stay flat, it is not doing much work. Good decision rules narrow the workflow before volatility speeds up and before the trader starts negotiating with the setup in real time.

Rule 1: Mean reversion works best when price is stretched relative to value, structure, or volatility and the trend is no longer cleanly expanding

If mean reversion works best when price is stretched relative to value, structure, or volatility and the trend is no longer cleanly expanding, define what qualifies as stretch before the session using structure, VWAP, volatility, or range context.

Why it matters: Higher timeframes define location; lower timeframes refine entry, stop placement, and timing

If the rule cannot be checked quickly in the live workflow, tighten it until the decision is obvious from the note, chart, or payload.

Rule 2: The edge comes from context and confirmation, not from a desire to pick tops or bottoms

If the edge comes from context and confirmation, not from a desire to pick tops or bottoms, require evidence of slowing continuation, rejection, or failure to hold the extreme.

Why it matters: Fast spikes matter less than whether price can hold the new area long enough to change the auction

A strong rule is one the operator can verify in seconds without inventing missing context.

Rule 3: The strongest mean-reversion trades usually happen in balanced markets, overextended bursts, or failed breakouts

If the strongest mean-reversion trades usually happen in balanced markets, overextended bursts, or failed breakouts, keep the invalidation clear so the trade is exited where the fade premise is actually wrong.

Why it matters: The stop distance has to reflect the product and volatility, but the invalidation must still sit where the read is wrong, not where the trade size looks prettier

If the rule still needs interpretation under pressure, the workflow is not ready for normal size.

Rule 4: A stretched move can stay stretched longer than an impatient trader expects

If a stretched move can stay stretched longer than an impatient trader expects, define what qualifies as stretch before the session using structure, VWAP, volatility, or range context.

Why it matters: Mean reversion needs a real reference for what counts as stretched

Use the rule to narrow the action set before the market accelerates, not to explain the trade afterward.

Key parameters and ranges to define before the session

Strong trading tutorials surface the numbers early. They make the trader define the range, threshold, or constraint before the trigger gets attention.

Table 1: Working ranges and thresholds

| Item | Working range | Why it matters |

|---|---|---|

| Top-down timeframe stack | Daily or 60-minute for location, 5-minute or 1-minute for execution | Higher timeframes define location; lower timeframes refine entry, stop placement, and timing. |

| Example confirmation window | 2 closes or 5 to 15 minutes of acceptance beyond a key level | Fast spikes matter less than whether price can hold the new area long enough to change the auction. |

| Example intraday invalidation distance | 4 to 8 ES points or 16 to 32 ticks beyond the reference | The stop distance has to reflect the product and volatility, but the invalidation must still sit where the read is wrong, not where the trade size looks prettier. |

| Stretch requirement | Price should be extended relative to value, range, or volatility | Mean reversion needs a real reference for what counts as stretched. |

| Failure confirmation | Look for rejection, reclaim, or inability to continue at the extreme | A large move alone is not enough. |

| Risk rule | The invalidation sits where the extension proves it is still alive | The stop belongs to the failure read, not to hope. |

These numbers should be written before the trade so they can shape the decision while the market is still moving, not after the fact. Read the item column first, then use working range to decide whether the setup still deserves risk, needs smaller size, or should be skipped outright.

Step-by-step implementation

Use the topic in this order so the decision stays clear before the market starts moving too fast to improvise cleanly.

Step 1: Define what qualifies as stretch before the session using structure, VWAP, volatility, or range context

Define what qualifies as stretch before the session using structure, VWAP, volatility, or range context. This step should remove one source of ambiguity before the trade is active.

Rule to verify here: Mean reversion works best when price is stretched relative to value, structure, or volatility and the trend is no longer cleanly expanding. If that is not true, define what qualifies as stretch before the session using structure, VWAP, volatility, or range context.

Useful range or threshold: Top-down timeframe stack -> Daily or 60-minute for location, 5-minute or 1-minute for execution. Higher timeframes define location; lower timeframes refine entry, stop placement, and timing.

Write down what would cancel this step before the trade goes live so the review can later confirm whether the gate was respected.

Step 2: Require evidence of slowing continuation, rejection, or failure to hold the extreme

Require evidence of slowing continuation, rejection, or failure to hold the extreme. Do not move on until the evidence for this step is visible in the chart, note, or payload.

Rule to verify here: The edge comes from context and confirmation, not from a desire to pick tops or bottoms. If that is not true, require evidence of slowing continuation, rejection, or failure to hold the extreme.

Useful range or threshold: Example confirmation window -> 2 closes or 5 to 15 minutes of acceptance beyond a key level. Fast spikes matter less than whether price can hold the new area long enough to change the auction.

Note the condition that would invalidate this step so the trader is not negotiating with it mid-trade.

Step 3: Keep the invalidation clear so the trade is exited where the fade premise is actually wrong

Keep the invalidation clear so the trade is exited where the fade premise is actually wrong. If this part stays fuzzy, the trade usually becomes harder to review honestly later.

Rule to verify here: The strongest mean-reversion trades usually happen in balanced markets, overextended bursts, or failed breakouts. If that is not true, keep the invalidation clear so the trade is exited where the fade premise is actually wrong.

Useful range or threshold: Example intraday invalidation distance -> 4 to 8 ES points or 16 to 32 ticks beyond the reference. The stop distance has to reflect the product and volatility, but the invalidation must still sit where the read is wrong, not where the trade size looks prettier.

If the evidence for this step disappears, the workflow should have a documented fallback instead of a guess.

Setup checklist and parameter table

Strategy articles need explicit setup logic. This section turns mean reversion trading strategy into a checklist with parameters the trader can review before the trade starts moving.

Table 1: Market-structure parameters to predefine

| Parameter | Example value | Why it matters |

|---|---|---|

| Primary reference | Prior value high | Gives a location that can attract or reject price |

| Confirmation rule | Two 5-minute closes above the level | Separates acceptance from a one-bar spike |

| Execution timeframe | 1-minute to 5-minute chart | Keeps lower timeframe work focused on entry and risk only |

| Invalidation distance | 4 to 8 ES points | Defines where the read is clearly wrong |

Writing parameters down before the open reduces hindsight-driven chart interpretation. Read the parameter column first, then use example value to decide whether the setup still deserves risk, needs smaller size, or should be skipped outright.

Table 2: Mean reversion setup table

| Requirement | What traders look for | Why it matters |

|---|---|---|

| Stretch | Distance from value, VWAP, or prior balance | Defines why the move may revert |

| Failure signal | Reclaim, rejection, or inability to continue | Prevents blind fading |

| Return path | Clear route back toward value | Improves target logic |

The edge comes from stretch plus failure, not from stretch alone. Read the requirement column first, then use what traders look for to decide whether the setup still deserves risk, needs smaller size, or should be skipped outright.

Entry confirmation and setup logic

A strategy guide should explain how the setup earns permission. For mean reversion trading strategy, that means spelling out the trigger sequence, the regime fit, and the condition that upgrades the idea from interesting to tradable.

Setup rule 1: Rule 1

Mean reversion works best when price is stretched relative to value, structure, or volatility and the trend is no longer cleanly expanding. Define what qualifies as stretch before the session using structure, VWAP, volatility, or range context.

If the condition is not visible before entry, the setup has not earned risk yet.

Setup rule 2: Rule 2

The edge comes from context and confirmation, not from a desire to pick tops or bottoms. Require evidence of slowing continuation, rejection, or failure to hold the extreme.

This rule should narrow the trade, not create another excuse to participate.

Setup rule 3: Rule 3

The strongest mean-reversion trades usually happen in balanced markets, overextended bursts, or failed breakouts. Keep the invalidation clear so the trade is exited where the fade premise is actually wrong.

The value of the rule is that it makes the failure condition obvious early.

Setup rule 4: Rule 4

A stretched move can stay stretched longer than an impatient trader expects. Define what qualifies as stretch before the session using structure, VWAP, volatility, or range context.

If this rule shows up late, the setup is usually weaker than it looks on replay.

Scenario walkthrough: worked trade example

A strategy guide should show the full trade path, not only the entry. For mean reversion trading strategy, the example should make the entry, stop logic, management plan, and failure response obvious while information is still incomplete.

Worked example 1: Intraday ES structure example

ES opens near prior value high after printing a 22-point overnight range, then tests the level twice in the first 30 minutes.

- Mark prior day high, prior day low, overnight high, overnight low, and the nearest balance edge before the open.

- Wait to see whether price accepts above value high for at least two 5-minute closes or rotates back inside the prior range.

- If the market holds the new area, use the lower timeframe to enter on a shallow pullback; if it fails back into value, treat the first breakout as noisy movement, not initiative control.

- Place invalidation beyond the level where acceptance would clearly be disproved, then compare the remaining distance to the next meaningful structural target.

The important part of this example is the decision chain. The decision should come from acceptance at location, not from raw speed or the first burst through a level.

A strong worked example should still be useful when the next chart looks different. The trader should be able to reuse the same sequence of checks, thresholds, and adjustments without needing the exact same screenshot to justify the decision.

That usually means the example leaves behind something reusable: a formula, a field check, an invalidation distance, a size adjustment, or a review prompt that can be copied into the next session plan with only the numbers changed.

Worked example 2: Fade after failed extension

A market stretches away from value into a prior extreme, fails to continue cleanly, and then reclaims the failed break area.

- Define the stretch relative to value or structure before the fade is considered.

- Wait for failure evidence such as rejection or reclaim rather than shorting the first fast push.

- Place the stop where renewed expansion would prove the fade wrong.

- Take profits or reduce when price rotates back toward value rather than demanding a full trend reversal.

The important part of this example is the decision chain. Mean reversion becomes safer when failure is confirmed before the fade is sized normally.

A strong worked example should still be useful when the next chart looks different. The trader should be able to reuse the same sequence of checks, thresholds, and adjustments without needing the exact same screenshot to justify the decision.

That usually means the example leaves behind something reusable: a formula, a field check, an invalidation distance, a size adjustment, or a review prompt that can be copied into the next session plan with only the numbers changed.

What the setup looks like in a live session

The point of a live walkthrough is to show the order of decisions while the information is still incomplete. That is what separates a practical trading article from a post-trade narrative.

Session moment 1

A trader sees price push far from value into a prior extreme and fail to continue cleanly. At this point the trader should be able to name the location, the condition that still makes the setup valid, and the line that would cancel it.

The useful question here is simple: Was the move stretched relative to something concrete? If the answer is still vague during the session, the trader usually needs to reduce size, wait for better evidence, or stay flat.

At this stage the operator should still be able to name the trigger, the invalidation, and the fallback response without opening a second chain of reasoning. If that answer needs storytelling, the workflow has already drifted away from the written plan.

Session moment 2

Instead of shorting immediately, the trader waits for failure evidence and a reclaim or rejection signal at structure. At this stage the trade should still have a clear reason to exist, a clear reason to stay inactive, and a clear reason to be abandoned if the read deteriorates.

The useful question here is simple: What evidence showed the trend was weakening? A fuzzy answer here is usually a sign that the setup should be downgraded, delayed, or ignored instead of forced.

The step is only useful if the trader can explain what would cancel the idea immediately, what would downgrade size, and what evidence would keep the plan intact under pressure.

Session moment 3

If the market re-accelerates and holds the extreme, the fade is invalidated instead of emotionally defended. This is the moment where the trader has to decide whether the evidence is improving the setup or simply making the chart busier.

The useful question here is simple: Was the fade taken into real balance or against strong continuation? If this question cannot be answered in real time, the workflow has probably moved faster than the written process can support.

This is also where the written process proves whether it is operational or decorative. If the trader cannot point to the exact field, level, or rule that controls the next action, the setup is still too loose.

Invalidation framework: when the read is wrong

A strategy stays honest when the trader knows which failure, reclaim, or lost condition proves the setup is no longer valid.

Metric 1: Top-down timeframe stack

Top-down timeframe stack matters because Higher timeframes define location; lower timeframes refine entry, stop placement, and timing.

- Working number: Daily or 60-minute for location, 5-minute or 1-minute for execution

- Why it changes the decision: Higher timeframes define location; lower timeframes refine entry, stop placement, and timing.

- How to use it: Translate top-down timeframe stack into the setup, the size, or the skip decision before the trade is live.

Write top-down timeframe stack into the plan before the session starts so the number can be checked without improvising.

Metric 2: Example confirmation window

Example confirmation window matters because Fast spikes matter less than whether price can hold the new area long enough to change the auction.

- Working number: 2 closes or 5 to 15 minutes of acceptance beyond a key level

- Why it changes the decision: Fast spikes matter less than whether price can hold the new area long enough to change the auction.

- How to use it: Translate example confirmation window into the setup, the size, or the skip decision before the trade is live.

If example confirmation window changes during the session, the trader should know exactly whether that means smaller size, slower timing, or no trade.

Metric 3: Example intraday invalidation distance

Example intraday invalidation distance matters because The stop distance has to reflect the product and volatility, but the invalidation must still sit where the read is wrong, not where the trade size looks prettier.

- Working number: 4 to 8 ES points or 16 to 32 ticks beyond the reference

- Why it changes the decision: The stop distance has to reflect the product and volatility, but the invalidation must still sit where the read is wrong, not where the trade size looks prettier.

- How to use it: Translate example intraday invalidation distance into the setup, the size, or the skip decision before the trade is live.

A useful metric becomes part of the review when the trader can compare the planned example intraday invalidation distance with what actually happened live.

Metric 4: Stretch requirement

Stretch requirement matters because Mean reversion needs a real reference for what counts as stretched.

- Working number: Price should be extended relative to value, range, or volatility

- Why it changes the decision: Mean reversion needs a real reference for what counts as stretched.

- How to use it: Translate stretch requirement into the setup, the size, or the skip decision before the trade is live.

The number should survive pressure because it already tells the desk what a valid, weak, or broken version of the setup looks like.

Metric 5: Failure confirmation

Failure confirmation matters because A large move alone is not enough.

- Working number: Look for rejection, reclaim, or inability to continue at the extreme

- Why it changes the decision: A large move alone is not enough.

- How to use it: Translate failure confirmation into the setup, the size, or the skip decision before the trade is live.

Write failure confirmation into the plan before the session starts so the number can be checked without improvising.

Metric 6: Risk rule

Risk rule matters because The stop belongs to the failure read, not to hope.

- Working number: The invalidation sits where the extension proves it is still alive

- Why it changes the decision: The stop belongs to the failure read, not to hope.

- How to use it: Translate risk rule into the setup, the size, or the skip decision before the trade is live.

If risk rule changes during the session, the trader should know exactly whether that means smaller size, slower timing, or no trade.

Troubleshooting and failure modes

This is where the topic usually breaks in real trading: not because the trader never heard the idea, but because the implementation drifted away from the rule.

Symptom 1: Fading a clean trend without evidence of exhaustion

Likely cause: Mean reversion works best when price is stretched relative to value, structure, or volatility and the trend is no longer cleanly expanding

Fix: Define what qualifies as stretch before the session using structure, VWAP, volatility, or range context

Correct the workflow before the next trade instead of writing a cleaner excuse for the last one.

Symptom 2: Calling any large candle overextended with no value reference

Likely cause: The edge comes from context and confirmation, not from a desire to pick tops or bottoms

Fix: Require evidence of slowing continuation, rejection, or failure to hold the extreme

The fix only counts if the next simulation proves the workflow changed in a measurable way.

Symptom 3: Using wide stops and vague exits that turn the fade into hope

Likely cause: The strongest mean-reversion trades usually happen in balanced markets, overextended bursts, or failed breakouts

Fix: Keep the invalidation clear so the trade is exited where the fade premise is actually wrong

A troubleshooting note should end with a changed rule, not with a more flattering explanation.

When the topic should stay inactive

A strong guide should also tell the trader when the setup does not deserve capital. That is where the written rule often protects more money than the entry pattern itself.

No-trade filter 1

Fading a clean trend without evidence of exhaustion. If that condition is already visible before the order is sent, the cleaner decision is usually to pass, reduce size, or wait for a better version of the setup.

This filter matters most on the days when the trader is tempted to force the setup because the session is active but not actually clean.

A no-trade filter is part of the edge because it protects the conditions that make the next clean setup worth trading. If the filter is already broken before entry, the account usually benefits more from preserved capacity than from another forced attempt.

No-trade filter 2

Calling any large candle overextended with no value reference. When that condition is already obvious, the setup is usually stronger as a no-trade decision than as a forced entry.

Most avoidable damage starts here, when a trader knows the condition is weak but still wants the label to count as permission.

This is where discipline protects future opportunity. Passing on a broken setup keeps capital, attention, and rule integrity available for the next trade that actually deserves them.

No-trade filter 3

Using wide stops and vague exits that turn the fade into hope. If this is already on the screen before the order is sent, staying flat usually protects more edge than arguing with the label.

The test is not whether the setup can be defended afterward. The test is whether it deserves capital while the evidence is still incomplete.

The practical job of this filter is to preserve decision quality. When the warning sign is already obvious before entry, protecting the account is usually the higher-value trade.

Live checklist and review framework

This section should leave the trader with a short list that can be used before the session and again after it. This is what keeps the topic actionable.

Before the trade

- Define stretch before the trade starts

- Wait for failure evidence, not just a large move

- Use a clear invalidation line

- Review whether the fade had context or was just impatience

After the session

- Was the move stretched relative to something concrete

- What evidence showed the trend was weakening

- Was the fade taken into real balance or against strong continuation

If the answers stay vague, the next revision should simplify the rule instead of adding another exception.

A good checklist section should shorten tomorrow’s decision, not just summarize today’s. The output of this review is usually one cleaner trigger, one clearer filter, or one narrower risk rule that makes the next live session easier to execute honestly.

That is also how the article becomes practical over time. The trader should be able to reuse the same before-trade checklist and after-session questions across multiple market conditions without rewriting the standard from scratch every time.

If the checklist cannot be copied into tomorrow’s prep and still make sense, it is probably summarizing the session instead of improving the process.

Bottom line

Mean reversion trading strategy: how traders fade stretched moves without catching a falling knife should give the trader a better live decision, not a better post-trade explanation. The durable version of this topic is the one that survives the note, the chart, the sizing rule, and the review without needing hindsight to make it look coherent.

If you remember only one thing, make it this: Mean reversion works best when price is stretched relative to value, structure, or volatility and the trend is no longer cleanly expanding Then check Top-down timeframe stack before sending risk. That combination usually does more to improve results than adding more opinions or more indicators.

The practical edge comes from documenting the workflow clearly enough that the next session starts with fewer assumptions, fewer avoidable mistakes, and a much cleaner answer to the question of whether the setup deserves risk at all.

That is the real standard for mean reversion trading strategy: the article should leave behind a rule the trader can execute, audit, and improve under pressure. If the write-up cannot survive a live checklist, a sizing worksheet, or a routing log, the idea is still too soft for capital.

The version worth keeping is usually not the most complicated one. It is the one that helps the trader make the next real-time decision faster, with fewer assumptions, clearer failure points, and a better reason either to take the trade properly or to stay out of it completely.

If the article did its job, the trader should be able to carry one or two lines from it straight into the next plan: the condition that proves the setup, the condition that cancels it, and the response that protects capital when the read weakens. That is the difference between helpful trading guidance and content that only sounds disciplined.

Frequently asked questions

Why is mean reversion hard for active traders?

Because stretched price can keep stretching. Without context and failure evidence, traders can fade strength long before the move is actually done.

What helps mean reversion most?

Value references, structure, volatility context, and clear failure signals usually help far more than simple overbought-overbought labels.

When does mean reversion work best?

It often works best in balanced markets, failed breakouts, and stretched moves that have already lost clean continuation quality.

Newer

Donchian channel breakout strategy: how trend-followers use channel breaks, pullback management, and exit rules

Older